Bengaluru, NFAPost: According to the International Data Corporation’s (IDC) Worldwide Quarterly Mobile Phone Tracker, India shipped 161 million smartphones in 2021. This was up by 7% YoY (year-over-year), even as supply and pandemic related challenges created disruptions during the year.

2021 started strong with pent-up demand from 2H20 (Jul- Dec)and positive sentiments around vaccinations but a severe second wave of Covid-19 dealt a blow to the growth. Constrained supplies resulted in low inventories across channels in the second half of the year, which usually has a high demand during the festive season.

According to IDC, the first quarter of the calendar year (Jan-Mar 2022) is expected to remain flat YoY amidst a low seasonal demand and a mild impact of the ongoing third wave of Covid-19, which will give the brands time to replenish their inventories.

The transition from 4G to 5G will continue to drive growth, though still restricted to mid and high-tier price segments.

Commenting on the development, IDC India Research Manager Client Devices Upasana Joshi said consumers continue to demand better features like the camera, battery, and processors over 5G capability in the entry-level price segments.

“The large feature phone base will remain crucial but elusive to the smartphone market in the absence of any affordable offerings at the entry-level,” said IDC India Research Manager Client Devices Upasana Joshi.

Key highlights of 2021 included:

With 81 million units, the online channel registered 13% YoY growth, surpassing the offline channel. This was driven by heavy marketing and initiatives like multiple sales festivals, attractive financing schemes, cashback & exchange offers, and trade-in programs. While the offline channel contracted in 2021, IDC expects offline shipments to recover some lost ground in 2022.

MediaTek-based smartphones recorded a 54% market share, creating a bigger lead over Qualcomm with more than 85% of its smartphones below US$200. UNISOC regained some momentum reaching a 7% share, up from 2% in the previous years.

ASPs peaked at US$190, growing by 15% annually. The share of the premium segment doubled from a year ago to 4% in 2021, growing by more than 100% annually, largely due to higher Apple shipments. The sub-US$100 was the only segment to decline YoY. IDC expects ASPs in 2022 to be high due to the rising cost of components and higher share of 5G smartphones.

IDC India Research Director, Client Devices & IPDS Navkendar Singh said overall, supply challenges and the second wave of Covid-19 severely restricted the market’s ability to achieve double-digit growth in 2021.

“Consumer demand is lower than expected as we entered 2022, but supply challenges are expected to ease by mid-2022, which should help in maintaining similar growth levels in 2022,” says IDC India Research Director, Client Devices & IPDS Navkendar Singh.

Top 5 Smartphone Vendor Highlights

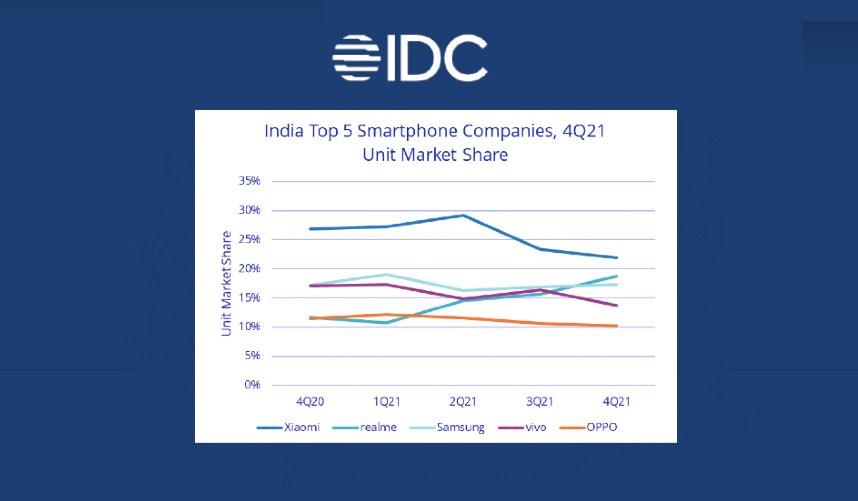

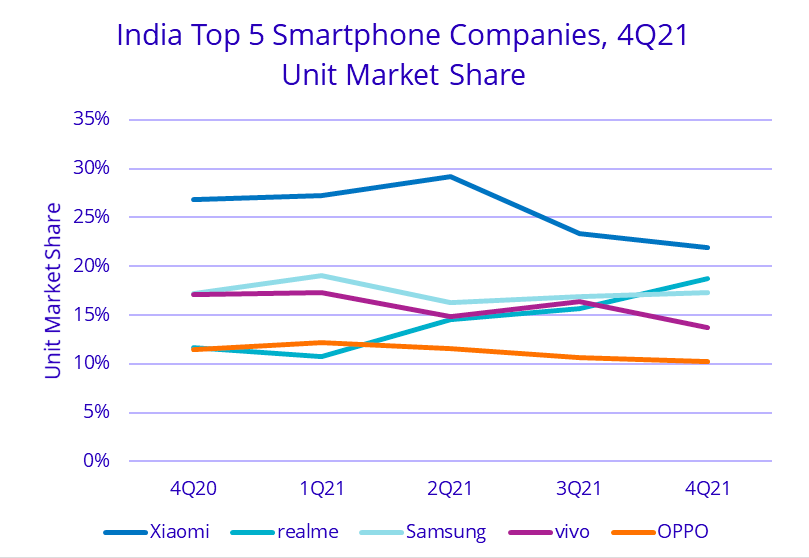

Xiaomi maintained its leadership position for four consecutive years with 40 million units, though declining by 1.5% YoY in 2021. Poco, Xiaomi’s sub-brand, emerged as the fastest growing online brand amongst the top five with 51% YoY growth. The entry-level models, Redmi 9A/9 Power/9, were the major volume drivers. Better supplies and a focus on offline channels should help drive growth for Xiaomi in 2022.

Samsung, at the second slot, registered a YoY decline of 6% in 2021, shipping 28 million units. There were persistent supply constraints especially for Galaxy A series in the low to mid-price segment, and for foldable devices in the premium segment. However, Samsung led the 5G segment with a 21% share, driven by the Galaxy A22, M32, and M42. A renewed focus on offline shipments in 2022, along with the momentum it has gained in the online segment, should help Samsung stay in a strong position in 2022.

vivo was at the third position, with a shipment decline of 6% YoY, though it continued to lead with a 28% share of offline channel shipments in 2021. Its Y series continued to be a major contributor, however, it faced supply challenges as well. vivo could leverage its sub-brand iQOO to expand its online presence and garner share in 2022.

realme at the fourth slot registered the highest growth of 26% YoY amongst the top 5 vendors. It also rose to the second slot in 4Q21 (Oct-Dec), surpassing Samsung, with a share of 19%. In the online space, it continued to be at the second slot with a high 21% share in 2021. realme’s UNISOC-based shipments reached 60% of its total, ensuring sufficient supplies in 4Q21.

OPPO, at the fifth slot, witnessed a healthy growth of 8% YoY in 2021 to 18 million units. It also surpassed Samsung for the second slot annually in the offline channel with a share of 18%. With a larger focus on higher ASP devices like the Reno 6/7 series, OPPO’s play in the mid-premium segment has risen compared to previous years. However, its online presence remains limited.