The 1st advance estimate (AE) of GDP for FY22 indicates GDP growth at 9.2% and GVA growth estimate is 8.6%. Nominal GDP growth is a whopping at 17.6%. Notably, this is the second-highest nominal growth achieved with 19.9% nominal growth registered in 2010-11 and 17.1% growth in 2006-07.

The data indicates that the overall GDP growth is 1% above of the pre-pandemic level (FY20). Almost all sectors except ‘trade, hotels, transport, communication & services related to broad- casting’ (which are still 8% below the pre-pandemic level) reached the pre-pandemic level (on constant prices). On the expendi- ture side, Private final consumption expenditure is still 3% below the pre-pandemic level.

Taking into account the revised GDP figures of today, even if we consider the additional spending announced by the Government in early Dec’21 fiscal deficit of the Government still comes at Rs 15.88 lakh crore or 6.8% of the GDP. For FY23, the fiscal consolidation should remain limited to 30-40 bps from the current fiscal.

Consequent of Omicron variant

Cases have been rising significantly in India as well as across the globe. However, studies so far reveal that the current Omicron variant is less severe than the Delta variant. Data also substantiates this fact. While number of new cases increased from 1.3 crore in Oct’21 to almost double to 2.5 crore in Dec’21 the number of deaths remained constant (just ~2200 more deaths occurred in Dec as compared to Oct).

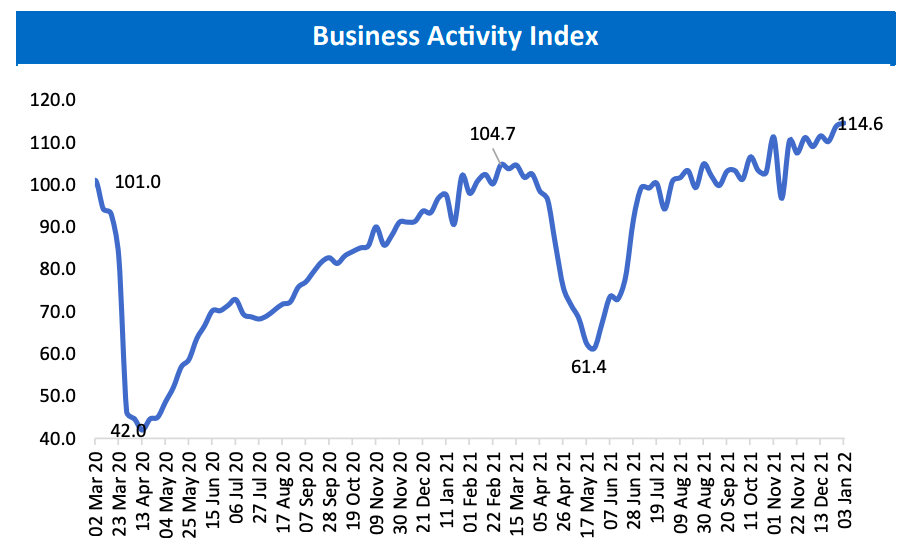

Even SBI business activity index is at its all time high of 114.6 for the week ended 3 Jan’21, indicating that economic activity is not getting affected by the sudden bout of infections. The index has been above the pre-Covid level since mid-Jul’21 barring some minor exceptions.

Going forward, we believe even if the rising infections could impact mobility, yet economic activity is not expected to get affected much. We believe that NSO’s estimate is on the conservative side, as the calculated GDP growth for H2 FY22 for construction comes at –0.9% and for Financing, insurance, real estate & bus. Services is at a mere 2.0% for H2 FY22.

We still believe that real GDP will grow at around 9.5% in FY22. Meanwhile, this estimate however has a shelf-life of only two months and is only used as an input for budget arithmetic. The NSO will release the first revised estimate of FY19, FY20 and FY21 on 31 Jan’21 and we believe that for FY22 the figures would be revised again in Feb’21 and May’21.

GDP ESTIMATED TO GROW BY 9.2% IN FY22

The 1st advance estimate (AE) of GDP for FY22 indicates GDP growth at 9.2% as compared to the contraction of 7.3%

in FY21. The GVA growth estimate is 8.6%. Nominal GDP growth is estimated to increase by 17.6% in FY22 vis-à-vis –

3.0% in FY21. We believe NSO has estimated the nominal GDP at a higher side, which may be around 14-15% in FY22.

NSO’s estimated GDP growth of 9.2% in FY22 is 30 bps lower than the RBI’s estimates. This indicates that NSO expect

5.6% GDP growth for H2 FY22, which seems quite conservative.

The data indicates almost all sectors except ‘trade, hotels, transport, communication & services related to broadcasting’ reached the pre-pandemic level (on constant prices). The above sectors are still 8% below the pre-pandemic level. On the expenditure side, Private final consumption expenditure is still 3% below the pre-pandemic level.

The per capita nominal GDP is expected to increase significantly. Compared to FY20, the NSO estimate of per capita GDP in FY22 is almost Rs 18,000 more.

Agri. and Allied Activities are likely to grow at 3.9% in FY22 as against previous year growth of 3.6%. This

expected as agriculture was only sector which was unscathed from the lockdown.

Industry, which was the most affected sector during lockdown, is estimated to grow by 11.8% in FY22 as compared to contraction of 7.0% growth in FY21 primarily due to low base and resumption of economic activities.

Service sector is likely to grow by 8.2% in FY22, compared to a degrowth of 8.4% in FY21, mainly due to the revival in the sector ‘Trade, hotels, transport, communication & broadcasting’.

The sub-segment ‘Financial, Real Estate & Professional Services’ growth is expected to increase by 4% in FY22, as compared to contraction of 1.5% in FY21. The estimated H2 FY22 growth in ‘Financial, Real Estate & Professional Services’ is only 2%, which seems very low, as the credit growth has shown momentum in H2.

The Public Administration sub segment is likely to increase by 10.7%, compared to last year de-growth

of 4.6%. In services, the most impacted sub-sector in FY21 ‘Trade, hotels, transport, communication & broadcasting’, is expected to grow by 11.9% compared to last year contraction of 4.6%.

On the expenditure side, all the components are expected to grow both in real and nominal terms mainly because of lower base of last year.

Government consumption is expected to witness higher growth of 7.6%, while private consumption expenditure growth is likely to pick-up to 6.9%. Gross fixed capital formation which took the largest brunt last year with double digit contraction also witnessed robust growth of 15%.

Positive growth in change in stocks entails that there has been an increase in inventory which is positive

for growth momentum.

On the external side, imports have grown higher than exports implying greater domestic absorption and investment demand.

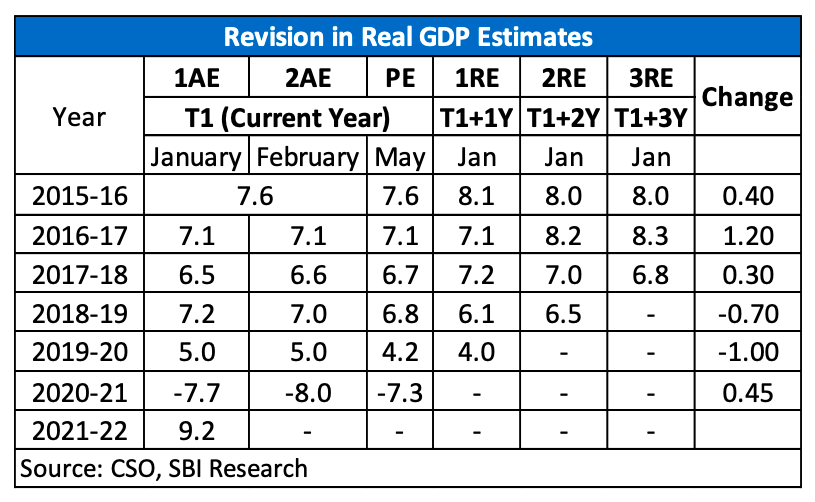

REVISION OF GDP NUMBERS

As we are aware, CSO releases the first estimates of any fiscal year in January and revises it first in February and again in May. So, it take almost 4-years (refer table) to publish the final data (1AE, 2AE, PE, 1RE, 2RE & 3rd RE).

Except, during FY19 & FY20, all years GDP data revision indicates an upward revision from the 1st AE released in January. However, in the current year FY22, we expect GDP numbers to be revised upwards and may come around 9.5% (SBI estimate for FY22).

GOVERNMENT EXPENDITURE & FISCAL SITUATION

Monthly data from CGA indicates that overall expenditure has already reached 59.6% of the BE till November 2021, with revenue expenditure at 61.5% of BE and capital expenditure at 58.5% of BE. This is lower than what was achieved last year. Capital expenditure has been falling for the past two months. In Oct-Nov’21, the government’s expenditure dropped 41.21% to Rs 44,279 crore compared to Rs 75,322 crore in the same period a year ago.

Meanwhile, higher revenues of the Government (69- 8% of the BE so far) enabled lower fiscal deficit at

46.2% of the BE till Nov’21, compared to 135% of BE till Nov’20. According to our calculations, total receipts of the Government would be higher than BE by around Rs 2.2 lakh crore.

Taking into account the revised GDP figures of today, even if we consider the additional spending announced by the Government in early Dec’21 fiscal deficit of the Government still comes at Rs 15.88 lakh crore or 6.8% of the GDP.

For FY23, the fiscal consolidation should remain limited to 30-40 bps from the current fiscal.

GRADUAL IMPROVEMENT IN CREDIT RATIO

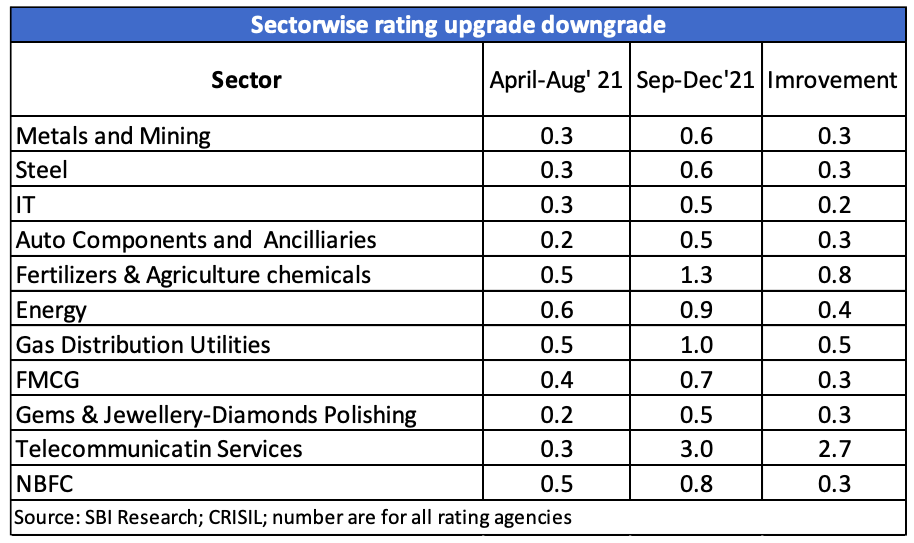

Credit ratio (upgrades/downgrades) show signs of improvement, albeit below one, in many sectors. During Sept-Dec’21, rating agencies reported 3531 downgrades as compared to 1216 upgrades, with a credit ratio of 0.34 against credit ratio of 0.27 during Apr-Aug’21 period.

Sectors which reported improved credit ratio include Metal, Steel, IT, Fertilizers & Agriculture chemicals, Energy, Telecommunications Services etc. Table below indicates some sectors where improvement in rating was observed:

WAY FORWARD

Cases have been rising significantly in India as well as across the globe. However, studies so far reveal that

the current Omicron variant is less severe than the Delta variant. Data also substantiates this fact. While number of new cases increased from 1.3 crore in Oct’21 to almost double to 2.5 crore in Dec’21 the number of deaths remained constant (just ~2200 more deaths occurred in Dec as compared to Oct).

Even SBI business activity index is at its all time high of 114.6 for the week ended 3 Jan’21, indicating that economic activity is not getting affected by the sudden bout of infections. The index has been above the pre-Covid level since mid-Jul’21 barring some minor exceptions.

Going forward, we believe even if the rising infections could impact mobility, yet economic activity is not expected to get affected much.

We believe that NSO’s estimate is on the conservative side, as the calculated GDP growth for H2 FY22 for construction comes at –0.9% and for Financing, insurance, real estate & bus. Services is at a mere 2.0% for H2 FY22.

We still believe that real GDP will grow at around 9.5% in FY22.