India Ratings and Research (Ind-Ra) has changed the outlook to improving from stable for retail non-banking finance companies (NBFCs) and housing finance companies (HFCs) for 2HFY22.

Adequate system liquidity (because of regulatory measures), along with sufficient capital buffers, stable margins due to low funding cost and on-balance sheet provisioning buffers, provides enough cushion to navigate the challenges that may emanate from a subdued operating environment.

This will lead to an increase in asset quality challenges due to the second covid wave impacting disbursements and collections for non-banks. The operating environment is dynamic due to the possibility of a third covid wave, its intensity, regulatory stance and its impact.

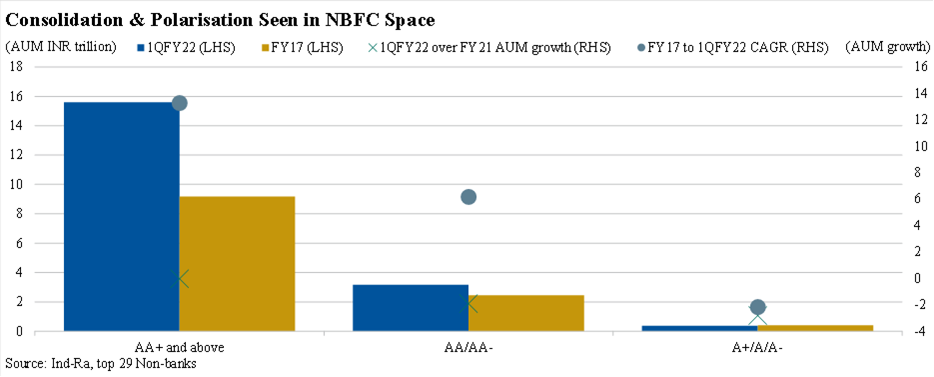

Ind-Ra believes in this environment, there is likely to be meaningful variations in the performance among different asset classes which would reflect on nonbanks depending on their assets under management mix.

NBFCs with a diversified asset mix and non-overlapping customer segments could be considered better placed to navigate operating challenges and may report a less volatile operating performance.

In FY22, Ind-Ra expects growth for NBFCs to be maintained in range of 9%-10%, in line with earlier stated expectations, and HFC growth could be maintained at 10%.

Incrementally, Ind-Ra believes diversification in product lines remains crucial for nonbanks to drive growth during cyclical downturns and have a wider product basket that negates the risk of single asset class franchise.

Growth in the commercial vehicle segment remains challenged, whereas certain sub-categories of vehicle finance such as tractors and small commercial vehicle financing could sustain their growth momentum during 2HFY22.

The gold segment, which witnessed reasonable growth due to rising gold prices in FY21, is likely to witness tapered growth in FY22, in the absence of a sharp pullback in prices. loan against property remains challenged where collateral values have been impacted due to the lack of resolution and challenges faced across micro, small and medium enterprises amid cash flow disruptions.

Lenders in the personal loan and business loan segments in the unsecured category are likely to be among the most impacted asset classes and lenders would remain cautious. Lenders are likely to look out for stronger borrowers and in this aspect, supply-chain financing, where their obligations remain on strong anchors, could gain traction.

The microfinance segment witnessed challenges during the second wave where the collection efficiency was impacted due to the wide spread nature of the pandemic in rural areas. Although collection efficiency and disbursements would improve, they will not without taking their toll in the form of elevated credit costs.

The funding costs for high-rated NBFCs have moderated, with frequent regulatory measures, along with continued on-tap targeted long-term repo operations. With system liquidity easing, rates have reduced; however, mobilising longer-tenor funds at competitive rates in the low-rated category remains challenging.

There has been a rise in co-lending partnership announcements across non-banks; even large HFCs are preferring to tie-up with well-established seasoned banks and other HFCs with granular liability profiles. Co-lending does help lenders to avoid cyclicality from fund mobilisation; however, the scaling of these channel needs to be monitored.

According to Ind-Ra’s assessment, asset quality for nonbanks had deteriorated in FY21, and there has been a further build-up in 1QFY22, keeping headline numbers elevated in FY22. The overall stressed book (gross non-performing assets + restructured book) for the top 10 NBFCs rose to 6.4% in FY21 from 5.4% in FY20.

Furthermore, the book’s benefit through the Emergency Credit Line Guarantee Scheme (ECLGS) would be around 5.1%, where there could be slippages post moratorium mostly in FY23. Similarly, HFCs witnessed a rise in delinquencies where the overall stressed book for the top 10 entities rose to 3.8% in FY21 from 2.3% in FY20.

The rise in delinquencies was high in 1QFY22 for NBFCs (top 10) and HFCs (top 10), where gross non-performing assets increased quarterly by 35% and 26.5%, respectively. Ind-Ra believes the segments facing heightened delinquencies for nonbanks are two wheelers, passenger vehicles, unsecured & secured business loans, microfinance and commercial vehicle. The agency believes these segments could remain under pressure for 2HFY22 as the business momentum remains subdued. The housing and gold finance segments have been more resilient to the pandemic and would continue to be so over the medium term.

As the overall stress on the loan book is on the rise, loss given default could increase if resolutions delays take longer than envisaged. Due to the pandemic, there were frequent lockdowns across states, leading to difficulties in the enforcement of hard collateral and the possibility of a resolution through Section 13(2), SARFESAI or through debt recovery tribunals.

Ind-Ra believes the reduction in cost due to the lockdowns imposed during the second covid wave would reverse when the rate disbursements increases. However, some reduction can be structural in nature which will could persist with the increased use of digital channels.

NBFCs are well capitalised to withstand any impact due to the fluid operating environment. Larger NBFCs have raised equity capital over the past 1-1.5 years and smaller NBFCs were anyways less levered. So, from a stress case perspective, the buffers are adequate to absorb any asset quality shock, Ind-Ra said.