India’s Smartphone Market Returns to Normalcy Towards the End of the Quarter, Clocking 34-million-unit Shipments in 2Q21, says IDC

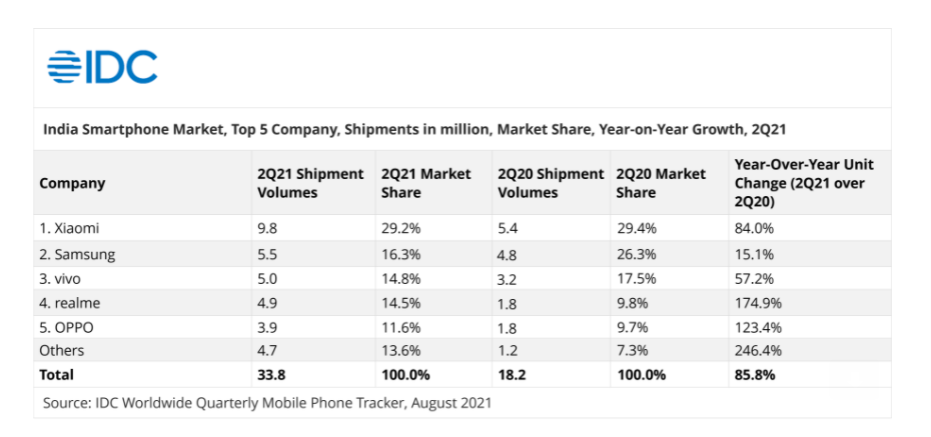

New Delhi, NFAPost: According to the International Data Corporation’s (IDC) Quarterly Mobile Phone Tracker, India’s smartphone market started 2Q21 (April-June) on a low note amidst the second wave of COVID-19 but quickly recovered towards the end of the quarter, witnessing 86% year-over-year (YoY) growth to reach 34 million units.

The second wave of COVID-19 hit the country almost a year after the first wave but varied significantly in terms of market response. Infections spread much faster even in rural areas and had a higher mortality rate, but there was a lesser impact on manufacturing and logistics, while the lockdown was not as strict as the year before.

As a result, state-led lockdowns resulted in a few pockets recovering faster in the second quarter, generating pent-up demand in June’21.

IDC India Research Director, Client Devices & IPDS, Navkendar Singh said while 2021 is expected to see single-digit growth, 2H21 is likely to drop in comparison to the same period last year, with lower demand, uncertainties around the third wave, persistent supply constraints, and rising component prices along with intensifying inflationary rates.

“Nevertheless, a rebound in 2022 will be possible with upgraders in the low-mid price segments, supply-led push of 5G devices, feature phone migration with new offerings expected in upcoming months (as announced by Reliance Jio), and better supplies to market,” says Navkendar Singh.

The key market trends for 2Q21 included:

Accelerated growth of the online channel, led by eTailers, resulted in a record share of 51% with a massive 113% YoY growth. On the flip side, the offline channel was impacted by weekend curfews in many areas and partially opened markets (with odd/even schemes) through May and mid-June.

MediaTek-based smartphones continued to lead with a share of 64% in sub-US$200, while Qualcomm dominated the space in the US$200-500 segment with a 71% share.

India stood at fourth position, following PRC, USA, and Japan, in terms of 5G shipments of 5 million with the lowest ASP at US$410. Though the government is yet to roll out the spectrum, IDC expects an inflow of more affordable 5G devices by end-2021 at sub-US$200.

Overall ASPs surged to a high of US$184, growing by 15% YoY. Price hikes and an ongoing shift to 5G in upcoming quarters drives ASPs to peak in 2021/2022.

IDC India Associate Research Manager, Client Devices, Upasana Joshi said though there were aggressively priced 5G model launches in 2Q21, most shipments were 4G.

“Nevertheless, it is still months away from 5G to become mainstream, underlining the importance of spectrum availability, clear use cases, and ensuring a cohesive future-ready infrastructure led by telcos,” says Upasana Joshi.

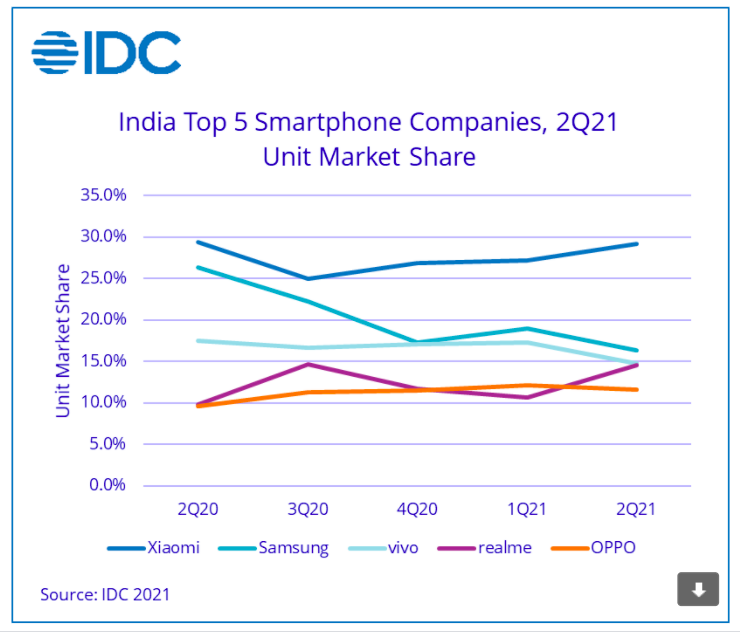

Top 5 Smartphone Vendor Highlights

Xiaomi led with an impressive 84% YoY growth. POCO, Xiaomi’s sub-brand, emerged as the fastest-growing brand nationally, despite a smaller model portfolio and being exclusive to Flipkart. Xiaomi commanded a 40% online market share with almost 70% of its shipments in online channels. Also, Xiaomi surpassed Samsung for the third slot in the offline channels with an 18% market share.

Samsung was second, registering the lowest YoY growth amongst the top 10 vendors at 15% in 2Q21. The vendor faced severe supply shortages. Its offline channel remained muted with a 4% decline, but its online shipments grew by 46% YoY, accounting for 49% of its total shipments.

vivo came at the third position, with 57% YoY growth. Though it continued to remain offline-heavy, it had new launches under the iQOO series, which were online-led. With 64% growth in the offline channel, vivo continued to command a majority share with its affordable Y series.

realme surpassed OPPO for the fourth slot with shipment growth of 175% YoY in 2Q21. It also overtook Samsung for the second slot within the online space with a 19% share, offering affordable 4G/5G models. Amongst the top 5 vendors, realme had the highest 5G contribution and led the space with a 23% share in 2Q21.

OPPO slipped to the fifth slot, but with shipment growth of 123% YoY in 2Q21. 17% of OPPO shipments were 5G, claiming third place in the 5G market after realme and OnePlus. It also surpassed Samsung for the second slot in offline channels at a 20% market share.