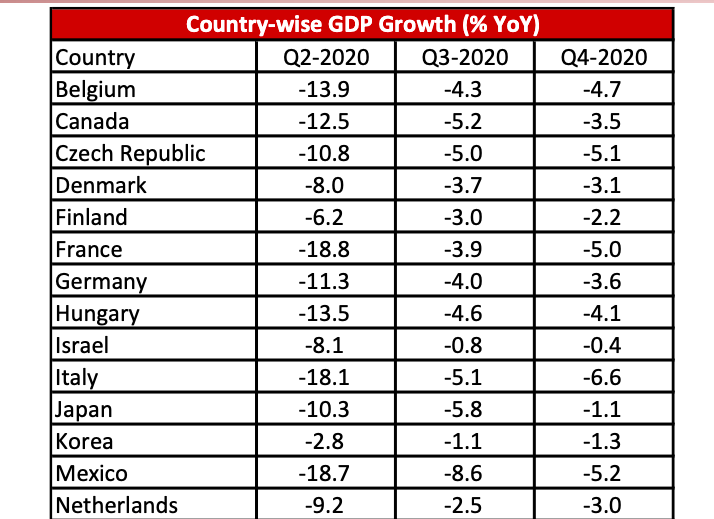

The economy contracted 24.4% in Q2 and 7.3% in Q3.

India is one of the few major economies to post growth in the last quarter of the calendar year 2020

The postulated Q4 FY2021 GDP decline a statistical aberration reflecting expenditure clean up

India’s economy exited the recession and registered a slight growth of 0.4% in Q3 FY21 after contracting 24.4% in Q2 and 7.3% in Q3, states SBI research report.

India is now one of the few major economies to post growth in the last quarter of the calendar year 2020, with improvement in the economy’s performance inversely tied to a drop in Covid-19 infections (even in most of the European economies the GDP contraction became deeper in Q4 2020 as compared to Q3

2020).

But as India has seen an uptick in cases over the last few weeks, it has raised the risk of a new round of localised lockdowns. New curbs on the movement of people or restrictions on businesses are a risk to the nascent recovery, given that gains in Q3 quarter probably came from the reopening of the economy.

Q4 GDP growth is however estimated to decline in Q4 FY21 because of a statistical aberration with food subsidy clean

up. GVA for Q4FY21 is at 2.7% and it is a better estimate to gauge economic recovery in the current background when tax numbers are notoriously fickle.

Decline in indirect tax

For the full fiscal GDP growth is expected to decline by 8.0% and GVA growth by 6.5%. For FY22, we still expect that real GDP growth would be around 11% and nominal GDP at 15%.

Normally the gap between annual GDP and GVA is less than 70 bps. For the first time in FY21 the gap is a whopping 148 bps primarily due to a huge decline in net indirect taxes in Q1 (in Q1 the gap was 200 bps).

The nominal loss of Rs 13.2 lakh crore in H1 has turned into gain of Rs 2.7 lakh crore in Q3 and is expected to be around Rs 2.8 lakh crore in Q4. For the entire fiscal, the nominal loss would be around Rs 7.6 lakh crore, though we believe that FY21 loss would be still less than the NSO estimate.

Agriculture & Allied activities grew by 3.9% in Q3 FY21 as compared to 3.4% growth in Q3 FY20. For FY21, agriculture is expected to increase by 3.0% as against 4.3% growth in FY20. Industry sector grew by 2.7% in Q3 primarily due to 7.3% growth in Electricity, Gas, Water Supply & other utility services and 6.2% in Construction.

Mining & Quarrying is still in negative territory. For FY21, the industry sector is expected to contract by 8.2% as against 1.2% decline in FY20. Electricity, Gas, Water Supply & other utility services is the only sector except for Agriculture which is expected to grow in FY21.

In Q3FY21, the services GDP growth, although negative, has recovered significantly to –1.0%, compared to a decline of –21.4% in Q1 and –11.3% in Q2, mainly due to rise in ‘Financial, Real Estate and Professional Services’, with growth at 6.6%. For FY21, services sector is expected to contract by 8.1% as against 7.2% growth in FY20.

The GDP deflator growth for FY21 is estimated at 4.6%, showing a 100 bps increase from FY20. However, going forward the real GDP growth is expected to turn positive and deflator is expected to come down again.

Overall, there is upward push in manufacturing, construction and trade, hotels, transport, communication & services related to broadcasting deflator and these are the sectors which have shown the highest GVA decline.

Investment scenario

The real and nominal gross fixed capital formation growth has turned positive in Q3, which is a good sign and hopefully, it will translate into better credit demand. Investment scenario, which can be better gauged by the actual tenders floated than announcements, reflects improved optimism in the last quarter (i.e., Q3FY21) with a number of tenders published increasing by 23% by numbers and 16% by the amount as compared to Q2FY21.

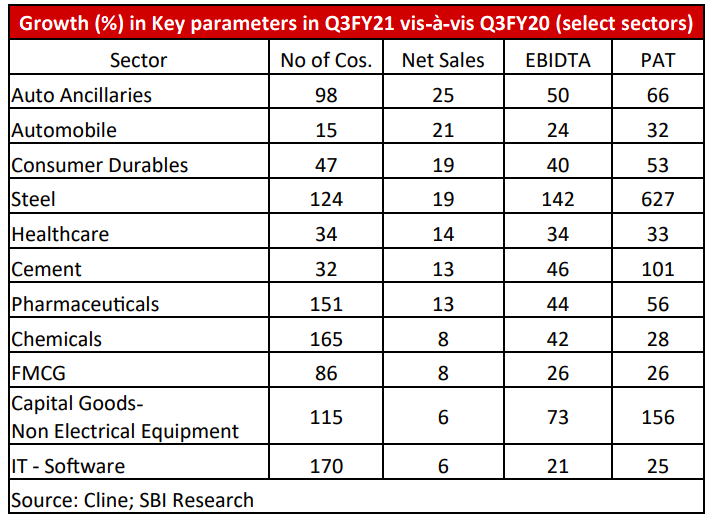

Overall, 12240 tenders were published in Q3FY21 with an amount of Rs 2.14 lakh crore. Corporate, in the listed space, reported better growth numbers across parameters in Q3FY21, as compared to Q3FY20, after improved EBIDTA in Q2FY21 post a dragged Q1FY21.

While analysing more than 3000 listed entities, excluding BFSI and refineries, we observed around 5% growth in top line and around 40% growth in EBIDTA. Profit After Tax (PAT) too grew by more than 60% in Q3FY21 as compared to Q3FY20. Sectors such as Automobile, FMCG, Pharma, Cement, Steel, Consumer Durable etc. reported better growth number in all key parameters.

With IIP manufacturing growth to remain in the positive territory in Q4 FY21 and bank credit showing robust growth in January, growth will continue to show some traction. Private final consumption is also expected to grow in Q4 FY21 by 3.1% in constant terms. Most importantly, there is a 2x improvement in rating upgrades during Sept’20 to Jan’21 period as compared to April to Aug’20 period, indicating continued improved incorporate rating profile.

Journey begins without recession

India’s economy exited the recession and grew by 0.4% in Q3 FY21 after contracting 24.4% in Q2 and 7.3% in Q3. For the full fiscal GDP growth is expected to decline by 8.0% and GVA growth by 6.5%. For FY22, we still expect that real GDP growth would be around 11% and nominal GDP at 15%.

Normally the gap between annual GDP and GVA is less than 70 bps. For the first time in FY21 the gap is a whopping 148 bps primarily due to a huge decline in net indirect taxes in Q1 (in Q1 the gap was 200 bps).

The nominal loss of Rs 13.2 lakh crore in H1 has turned into a gain of Rs 2.7 lakh crore in Q3 and is expected to be around Rs 2.8 lakh crore in Q4. For the entire fiscal, the nominal loss would be around Rs 7.6 lakh crore, though we believe that FY21 loss would be less than the NSO estimate.

Agriculture: As expected Agriculture & Allied activities grew by 3.9% in Q3 FY21 as compared to 3.4% growth in Q3 FY20. For FY21, agriculture is expected to increase by 3.0% as against 4.3% growth in FY20.

Industry: The growth in the Industry has turned positive in Q3 after plunging –35.9% in Q1. The industry sector grew by 2.7% in Q3 primarily due to 7.3% growth in Electricity, gas, water supply & other utility services and 6.2% in construction. Mining & quarrying is still in negative territory. For FY21, the industry sector is expected to contract by 8.2% as against 1.2% decline in FY20. Electricity, gas, water supply & other utility services is the only sector except for Agriculture which is expected to grow in FY21.

Services: In Q3FY21, the services GDP has recovered significantly to – 1.0%, compared to a decline of –21.4% in Q1 and –11.3% in Q2, mainly due to a rise in ‘Financial, Real Estate and Professional Services’, with growth at 6.6%.

Despite GDP growth turning positive, the total final consumption expenditure growth was negative in Q3 FY21 in constant terms. However, the pace of decline has significantly moderated. And, the total real final consumption expenditure growth is estimated to turn positive in Q4 FY21, led by double-digit growth in government final consumption expenditure. Private final consumption is also expected to grow in Q4 FY21 but only by a meagre 3.1% in constant terms, and that too due to

a lower base in Q4 FY20. However, in current terms from Q3 onwards the total final consumption expenditure growth has turned positive.

Gross fixed capital formation constant growth rate which had

turned negative in Q2 FY21 turned positive in both real and nominal terms, which is a positive sign. Some push has been given to growth by restocking as evident from its growth. Exports and imports decline has persisted in Q3 as well as Q4.

The GDP deflator growth for FY21 is estimated at 4.6%, showing a 100 bps increase from FY20. However, going forward the real GDP growth is expected to turn positive and deflator is expected to come down by 100 bps again. If we look at the sector-wise data, the agri deflator growth was much higher than the GDP growth pre-pandemic. However, now the real GVA growth surpasses the deflator growth albeit marginally. For industry, the GVA growth and deflator were showing a similar trend pre-pandemic. But from Q1 FY21 there was a sharp decline in industrial growth while the deflator decline was moderate. From Q3 FY21 both deflator and GVA growth have picked up. In industry, manufacturing growth deflator had remained in negative territory in FY20 before turning positive in Q2 FY21. Construction sector deflator and GDP growth rate have followed a similar pattern. Meanwhile, electricity, gas and utility GVA growth has been much higher than the deflator growth post-pandemic. The services sector deflator climbed up from the time the pandemic started. In the travel, tourism and other services, the deflator growth has in fact gone higher than the pre-pandemic growth, despite GVA growth decline in double digits.

Improvement in incremental credit

In the current year FY21 so far (up to 12 Feb’21), the ASCBs YoY credit growth data indicate an upward journey and touched

6.6% (vis-à-vis 6.4% in the corresponding period the previous year). Even on an YTD basis the ASCBs advances increased to 3.2% (Rs 3.3 lakh crore) in FY21, compared to last year YTD growth of 2.8% (Rs 2.7 lakh crore). Thus, this year’s incremental credit growth is 23% higher than the previous year actual numbers.

Recently, RBI released quarterly statistics on Deposits and Credit of SCBs, which indicates credit growth (YoY) improved to 6.2% in Dec’20 from 5.8% in the previous quarter but it remained lower when compared with 7.4% growth recorded a year ago; all population groups (i.e., rural, semi-urban, urban and metropolitan) recorded lower growth when compared to a year ago. Credit by private sector banks moderated significantly to 6.7% in Dec’20 (13.1% a year ago), whereas that for public sector banks improved to 6.5% in Dec’20 (3.7% in Dec’19). However, on a positive note that ASCBs incremental credit growth during Jan’21 showed robust growth in all most all the sectors.

The sectoral data for Jan’21, which accounts about 90% of the total bank credit deployed by 33 SCBs, indicates that the incre-

mental credit has jumped significantly in almost all the major sectors (Agri, Services, Industry & Personal Loans) in Jan’21. The

incremental credit growth during April-January, FY21 indicates

that credit off-take has been taken place in almost all the sectors

except industry and NBFC. The industry credit growth is declining

as they might be raising money from bond markets.

Within the industry, credit to ‘mining & quarrying’, ‘food processing’, ‘textile’, ‘gems & jewellery’, ‘petroleum, coal products & nuclear fuels’, ‘paper & paper products’, ‘leather & leather products, and ‘vehicles, vehicle parts & transport equipment’ registered accelerated growth in Jan’21 as compared to the growth in the corresponding month of the previous year. However, credit growth to ‘rubber plastic & their products’, ‘beverages & tobacco’, ‘chemicals & chemical products’, ‘basic metal & metal products’, construction’ and ‘infrastructure’ decelerated/contracted.

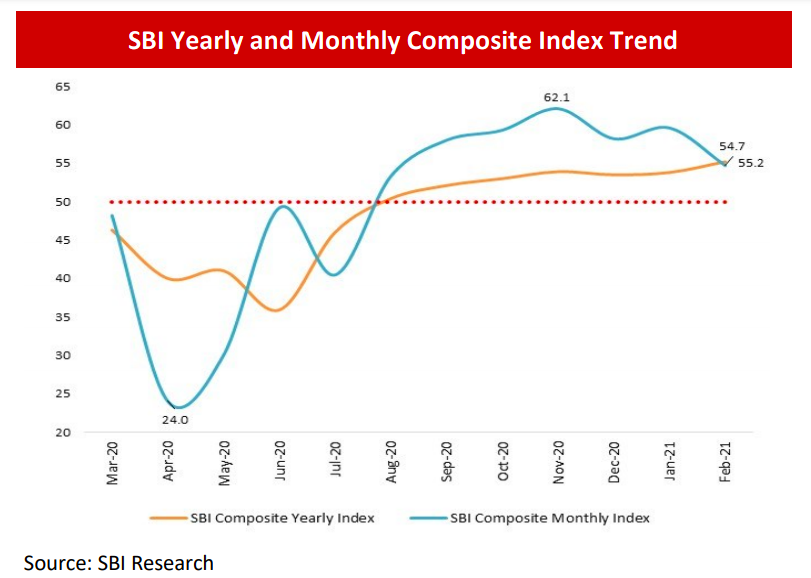

SBI YEARLY COMPOSITE INDEX

The yearly SBI Composite Index reached 22-month high of 55.2 (High Growth) in February 2021, compared to 53.8 (Moderate Growth) in Jan’21, and 51.1 (Low Growth) in Feb’20. However, the monthly index declined marginally to 54.7 (Moderate Growth) in Feb’21, compared to 59.6 (High Growth) in Jan’21 and 50.2 (Low Growth) in Feb’20. Based on the SBI index, we believe IIP & IIP manufacturing may grow 1.5-2% in Jan’21 and 2.5-3.0% in Feb’21.

Growth of corporates

Renewed optimism

Corporate, in the listed space, reported better growth numbers across parameters in Q3FY21, as compared to Q3FY20, after

improved EBIDTA in Q2FY21 post a dragged Q1FY21.

While analysing more than 3000 listed entities, excluding BFSI

and refineries, we observed around 5% growth in top line and around 40% growth in EBIDTA. Profit After Tax (PAT) too grew by

more than 60% in Q3FY21 as compared to Q3FY20. Sectors such as Automobile, FMCG, Pharma, Cement, Steel, Consumer

Durable etc. reported better growth number in all key parameters.

Reducing debt

It is also observed that share of loan funds of companies with

interest coverage of less than one, decreased to around 20% in

half-year ended Sept’20 as compared to 26% and 37% in half-year ended Sept’19 and March’20 respectively, reflecting better

loan serving capacity and efficient credit management.

Investment scenario

Investment scenario, which can be better gauged by the actual tenders floated than announcements, reflects improved optimism in the last quarter (i.e., Q3FY21) with a number of tenders published increasing by 23% by numbers and 16% by the amount as compared to Q2FY21. Overall, 12240 tenders were published in Q3FY21 with an amount of Rs 2.14 lakh crore.

In last 9 months i.e. April to Dec’20, around 28255 tenders were published with an overall amount of Rs 5.82 lakh crore as

compared to 17884 tenders with an amount of Rs 7.03 lakh crore

in the same period previous year suggesting 58% growth in the number and a 17% decline in value.

With an estimated infrastructure spending of more than Rs 5

lakh crore announced in the recent union budget in the sectors

such as Road, Rail, Power, Health etc., we expect the same to

increase further in FY22.

Improving credit ration

One of the indicators of improvement in corporate strength is their rating. While analysing rating for various sectors, we observed improvement in credit ratios post August’2020. In 26 major sectors, we say around 2x improvements in rating upgrades during Sept’20 to Jan’21 period as compared to April to

Aug’20 period. Overall, there are 899 upgrades and 4998 downgrades from Sept’20 to Jan’21 as compared to 462 upgrades and 5732 downgrades from April to Aug’20.

Country-wise GDP growth

India is now one of the few major economies to post growth in the last quarter of the calendar year 2020, with any improvement in the economy’s performance inversely tied to a drop in Covid-19 infections (even in most of the European economies the gdp contraction became deeper in Q4 2020 as compared to Q3

2020). But as India has seen an uptick in cases over the last few weeks, it has raised the risk of a new round of localised lockdowns. New curbs on the movement of people or restrictions on businesses are a risk to the nascent recovery, given that gains in Q3 quarter probably came from the reopening of the economy.