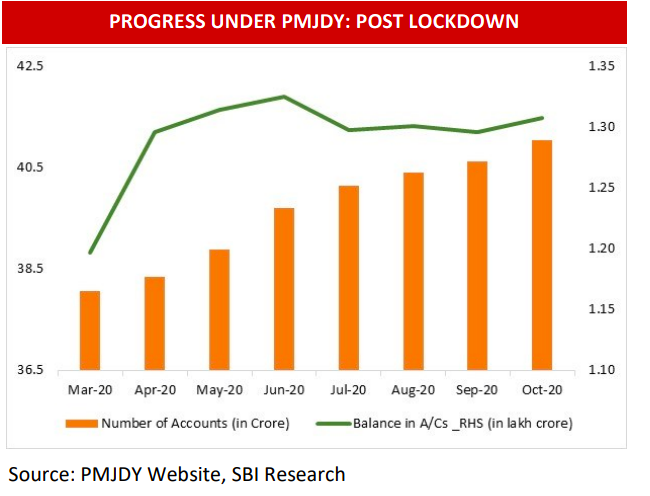

Bengaluru, NFAPost: As per the latest data on 14 October 2020, the total number of PMJDY accounts stood at 41.05 crore with a total balance of Rs 1.31 lakh crore, states a report published by SBI.

Since April 1, around 3.0 crore accounts were opened, with total rise in deposits of RS 11,060 crore in the PMJDY accounts. The pandemic has led to a 60% increase in the opening of new Jan Dhan accounts.

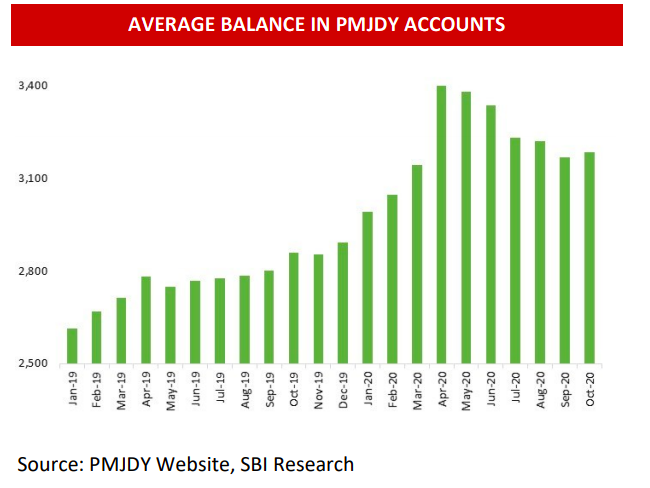

The average balance of PMJDY accounts increased to Rs 3400 in April and declined there after to Rs 3168 in September and now marginally increased to Rs 3185 in October 2020.

Thus, the initial increase in average balance that was primarily due to the loss of livelihood due to pandemic and shift of migrant labourers from urban areas to home resulting in jump of precautionary savings, may have been reversed.

Our activity index indexed at February at 100, which showed increased momentum in September continues to improve in October, with our latest reading slightly above 90, mainly because of higher RTO revenue collections and higher mobility as indicated by Google workplace mobility. This is however the most crucial phase!

Empirical research (Sumit Agarwal, Shaswat Alok, Pulak Ghosh, Soumya Kanti Ghosh etc., 2020 all) suggests that PMJDY accounts work as a primary vehicle for labour remittances, apart from increased lending, smoothing consumption, increased spending on healthcare and most importantly the usage is more frequent in areas that are more crime prone (once the data is juxtaposed with other sources of data).

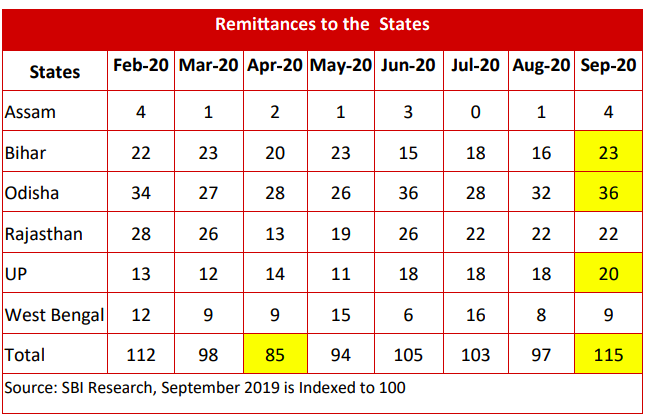

Subsequently, we looked at representative SBI sample data on labour remittances beginning September 2019. The actual data was normalised to 100 in September 2019 and thereafter adjusted accordingly. The data indicates that there was a significant reduction in remittances due to lockdown and it touched the lowest level in April.

However, it increased in June & July and in September it has just crossed the pre-COVID level as witnessed in February. Thus it seems migrant labourers are coming back in adequate numbers to workplaces for livelihood and that too much before Diwali as was largely expected.

Additionally, during Apr-Aug’20, 25 lakh new EPF subscribers have joined of which 12.4 lakh were first time payroll entrants. The point of concern though is that the degree of formalization has dropped significantly to 6% in FY21 from an average of 11% in earlier years. The increase in remittance though are in perfect coordination with increase in payroll. The jump in payroll leads to higher remittances.

As indicated, we also find evidence that the usage of PMJDY accounts increases over time in regions that are more prone to theft. Acknowledging that the genesis of crime can also be traced to interplay of various social, economic, demographic, local and institutional factors apart from putting more money in accounts at the lower strata of society, there is evidence of PMJDY accounts having some impact on crimes.

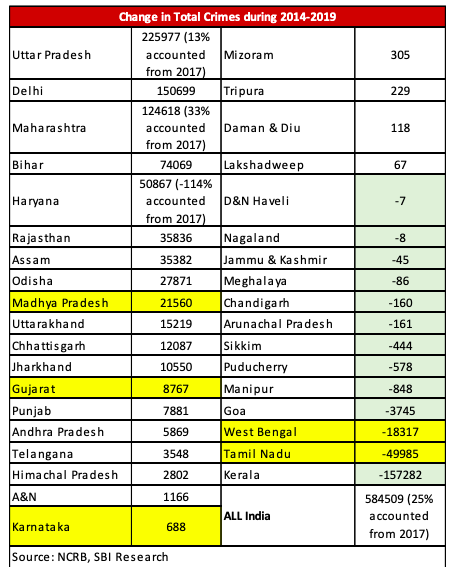

Thus, some of the states like Uttar Pradesh, Maharashtra and Haryana may have witnessed a lagged impact of the usage of PMJDY accounts and thus a positive impact on theft. States like West Bengal, Tamil Nadu and even Kerala have seen a continuous impact since inception. States like Gujarat and Karnataka have also seen a favourable impact.

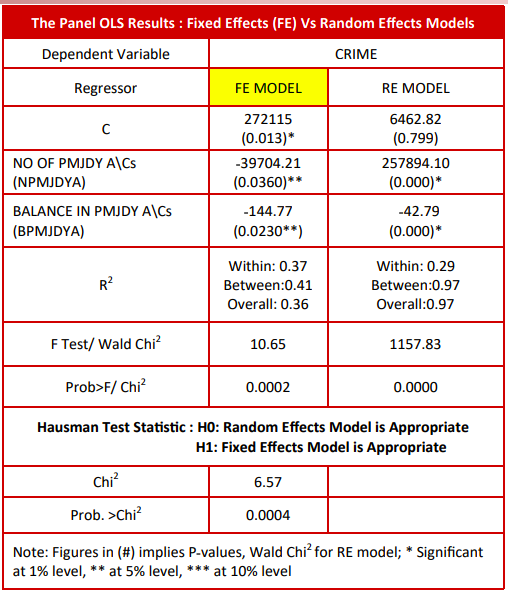

Interestingly, the panel data model we estimated also suggests that fixed effect are more important in our model. In economic parlance, fixed effects are variables that are constant across individuals; like age, sex, or ethnicity and don’t change or change at a constant rate over time. In other words, the usage of PMJDY that is causing the change in individual behavior is the same across all states and uniform across all!

We thus recommend that the Government should strive to put more money into such accounts as a sort of third fiscal stimulus, possibly through enlarging the NREGA scheme or through a scheme for urban poor. It is a matter of satisfaction that the usage of such PMJDY accounts in current unprecedented times has surely helped in maintaining social harmony.

PMJDY ACCOUNTS HAVE SURPASSED 41 CRORE

As per the latest data on 14 October 2020, the total number of PMJDY accounts stood at 41.05 crore with a total balance of ₹1,30,741 crore. Since April 1, around 3.0 crore accounts were opened, with total rise in deposits of RS 11,060 crore in the PMJDY accounts. During the same period in 2019, only 1.9 crore were added with increase in deposits of only Rs 7857 crore. Thus, the pandemic has led to a 60% increase in the opening of new Jan Dhan accounts.

We believe this surge is possibly related to the thrust on digital payments – which require a bank account – amid the rising fear of infection. Under the Atmanirbhar package, Government also credited the women PMJDY accounts Rs 500/a month, which we believe should have been continued at least till September. The average balance of PMJDY accounts increased to Rs 3400 in April and declined there after to Rs 3168 in September and now marginally increased to Rs 3185 in October 2020.

The initial increase in average balance was primarily due to the loss of livelihood due to pandemic and shift of migrant

labourers from urban areas to home to save the life that resulted in jump in precautionary savings.

Empirical research (Sumit Agarwal, Shaswat Alok, Pulak Ghosh, Soumya Kanti Ghosh etc., 2020 all) suggests that PMJDY accounts work as a primary vehicle for labour remittances, apart from increased lending, increased spending on healthcare and most importantly the usage is more in areas that are more crime prone indicating lower rate of crime once the data is juxtaposed with other sources of data. We use the results of this paper as our primary source of research for our current report.

LABOUR REMITTANCES JUMPED SMARTLY IN SEPTEMBER INDICATING RETURN OF LABOURERS AFTER REVERSE MIGRATION

Seasonal and circular migration is an integral livelihood strategy for poor people in India. In fact, over the years, migration has been an important livelihood option for both the poor and the non-poor in India. As a result of unequal growth, people from agriculturally and industrially less developed states migrate to more developed states in search of job opportunities – for example from Uttar Pradesh, Bihar, the southern part of Madhya Pradesh, Odisha, and Rajasthan to states like Punjab, Gujarat, and Maharashtra. For a large number of migrants, New Delhi is also a much favoured destination, due to the abundance of job opportunities.

To check the current trend, we looked at a representative SBI sample data on labour remittances (September 2019 indexed to 100). The actual data was normalized to 100 in September 2019 and thereafter adjusted accordingly which is presented in the adjacent table.

The data indicates that there was significant reduction in remittance numbers due to lockdown and touched the lowest

level in April. However, it increased in June & July but declined in August. The decline in August may be due to heavy rains that stopped work in many areas across the country. Further, in September it has crossed the pre-COVID level in February. This seems migrant labourers are coming back in large numbers tonthe workplace for livelihood.

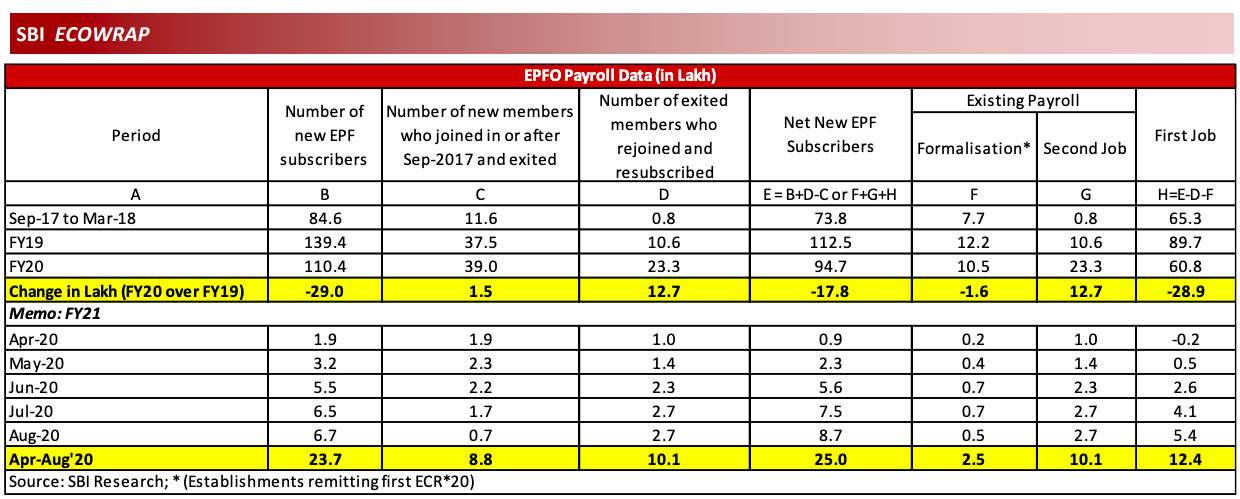

REMITTANCES WERE ALSO ACCOMPANIED BY MORE CRATION OF FIRST TIME PAYROLL JOBS IN AUGUST

Based on the payroll data provided by EPFO, during FY20 a total of 110.4 lakh new EPF subscribers were added as compared to 139.4 lakh in FY19 indicating a loss of 29 lakh subscribers.

However, during Apr-Aug’20, 25 lakh new EPF subscribers have joined of which 12.4 lakh were first time payroll entrants. The point of concern though is that the degree of formalization has dropped significantly to 6% in FY21 from an average of 11% in earlier years.

We define second job as the ‘exited members who rejoined and re-subscribed’ which was 10.1 lakh in Apr-Aug’20.

The increase in remittance are in perfect coordination with increase in payroll. The increasing payroll leads to higher

remittances.

SOCIAL BENEFITS OF PMJDY ARE MANY

Empirical research (Sumit Agarwal, Shaswat Alok, Pulak Ghosh, Soumya Kanti Ghosh etc., 2020 all) suggests that about 70% of the PMJDY accounts maintain a positive balance. While the initial usage remains quite infrequent, it gradually increases over time. Remittance is the most frequently occurring transaction. There is heterogeneity in usage across individuals based on age, marital status, and mobile ownership. Usage increases over time in regions that are more prone to theft. Banks also provide overdraft facility in PMJDY accounts, based on the ac- count usage, which is also counted under PSL requirements of the banks.

Though, Jan Dhan accounts has many positive aspects like saving habits, insurance coverage, OD facility etc. but it has also social implications. To study this aspect, we mapped the PMJDY accounts data with the state wise crime data.

Crime is manifestation of myriad complex factors. The causes of criminal behavior lie in the social processes and structures. People commit crimes due to the process of socialization that does not develop strong sense of right or wrong and due to the emerging opportunities, the enlarging desires that act as strong motivation for taking to crime to fulfill these desires. The genesis of crime can be traced to interplay of various social, economic, demographic, local and institutional factors.

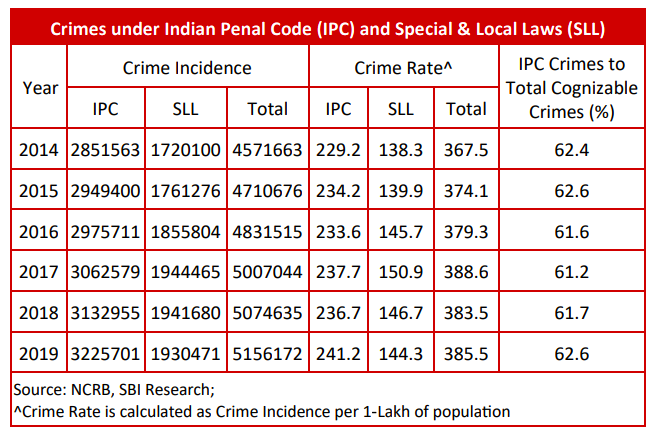

In India, over the years crimes has been increasing. In 2019, a total of 51.5 lakh cognizable crimes comprising 32.3 lakh IPC crimes and 19.3 Special & Local Laws (SLL) crimes were registered, with an increase of 1.6% in registration of cases over 2018 . Crime rate registered per lakh population has increased marginally from 383.5 in 2018 to 385.5 in 2019. Crimes against women and children has increased by 7.3% and 4.5% respectively in 2019.

As we had indicated, the balance in Jan Dhan accounts has a positive impact on crimes, related to theft. To see the impact of Jan Dhan accounts on crimes, we looked at the state wise data accounts level data of PMJDY both ‘No of accounts’ and ‘Balance’ and mapped with the state ‘number of total crimes’ from 2016 to 2020.

As crime data is available till 2019, so we had taken into account 37-states & UTs (including India) and 4-years data (2016-2019) to build a panel data model as :

CRIME = C + α PMJDY Accounts + β PMJDY A/C Balance + μ

The estimated results indicate that both Fixed Effects (FE) and Random Effects (RE) models are significant. However, the ‘Hausman Test’ results confirm that Reject H0, i.e. the FE model is appropriate. The FE model indicates that with the rise in num- ber of PMJDY accounts and balance in these accounts leads to fall in crime.

Interestingly, some of the states like Uttar Pradesh, Maharashtra and Haryana may have witnessed a lagged impact of the usage of PMJDY accounts and a positive impact on theft. Such lagged impact is proxied by the percentage contribution to incremental cases since 2014 but beginning 2017. If this number is small as is the case with Uttar Pradesh (only 13% increase since 2017 to overall number of crime), Maharashtra and even negative for Haryana there is clear evidence of PMJDY account usage resulting in perhaps reduced theft and thereby crime but with a lagged impact as people start using the accounts. States like West Bengal, Tamil Nadu and even Kerala however have seen a

continuous impact since inception. States like Gujarat and Karnataka have also seen favourable impact.