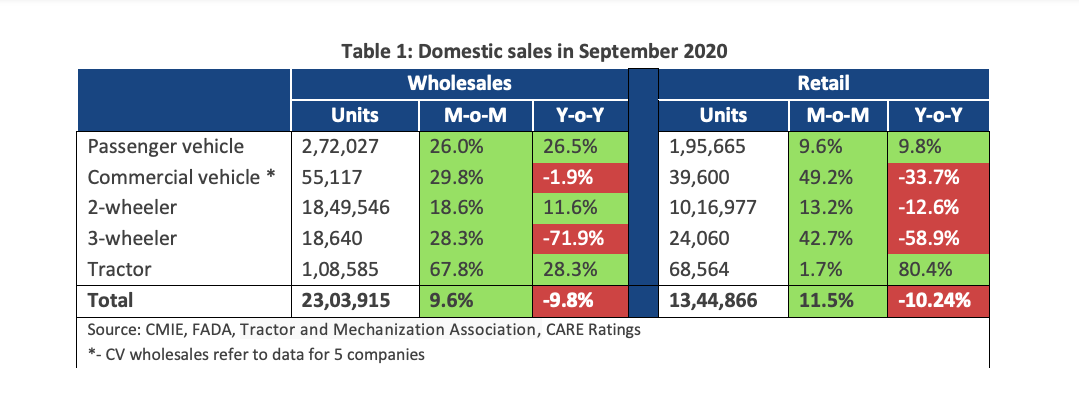

Bengaluru, NFAPost: September 2020 witnessed a sharp surge in domestic wholesales (sales by OEMs to dealers), not only sequentially, but also on YoY basis in segments like tractors, Passenger Vehicles (PVs) and 2-wheelers.

Due to an improvement in mining and infrastructural activities along with a pickup in the demand from the E-commerce sector, commercial vehicles saw a V-shaped recovery as the domestic sales in Q2-FY21 more than quadrupled sequentially.

Within the MHCV segment, sales of trucks were better than buses as demand from office, school and tourism segments remained soft. Tractors continue to be the best performing segment with domestic sales exceeding previous year levels by a high margin in 6M-FY21, except April 2020. The 3-wheeler segment has still not witnessed much signs of green shoots, as September 2020 domestic sales fell 71.9% YoY.

Consumer demand

Such strong growth wholesales numbers do hint at a recovery in the automotive sector. However the actual consumer demand which gets reflected in the retail sales data (sales by dealers to end consumers) is yet to gain some pace.

Analysis of the below table shows that the retail sales in September 2020 were substantially lower than the wholesales, which means that automotive OEMs are increasing production and pushing inventories to dealers in anticipation of the rise in demand during the upcoming festive season that starts 17th October onwards.

While all segments have witnessed sequential growth in retail sales, a comparison on a YoY basis shows that segments like CVs, 2 & 3-Wheelers are still witnessing high double-digit decline.

Currently, inventory for 2 wheelers (45-50 days) and PVs (35-40 days) are at the highest levels (according to FADA). Hence, if the festive season does not lead to rise in consumer demand, it may seriously dampen the financial health of automotive dealers, who are already surviving on thin margins.

Market share

The automotive OEM sector is highly concentrated and hence the top few players account for a majority of the market share. Within the 2 & 3-wheeler segments, 60% retail sales were made by top 2 players during the month, while in the CV segment top 2 players sold 66% of total units.

In the passenger vehicle segment, only 1 player accounts for exactly half the market share, while the following 2 players hold a quarter share. In the tractor segment, top 3 players, enjoyed 52% market share.

Geography wise sales: In absolute numbers, highest retail sales were recorded in Tamil Nadu with 1.7 lakh vehicles, followed by Uttar Pradesh with 1.67 lakh vehicles and Maharashtra with 1.53 lakh vehicles. Five large states: Tamil Nadu, West Bengal, Maharashtra, Karnataka and Kerala witnessed higher automotive demand in September 2020 when compared with previous year levels.

Ready for festive season

These five states account for a large portion of India’s economic output and as the economic activities gradually rose during the month, it helped in creating fresh demand for automobiles. Retail sales in Tamil Nadu, West Bengal and Maharashtra grew by 17.2%, 9.5% and 1.95 YoY respectively.

The festive season of this year will be even more critical for the automobile sector, as it has long been affected by low consumer sentiments even before the pandemic started.

To attract customers, automobile OEMs along with dealers have recently rolled out various offers such as cash discounts, extended warranty, maintenance programme, complementary accessories, additional benefits for loyal members, vehicle exchange offers, easy buying options in the form of long-tenure and easy EMI options, floater health insurance cover, etc.

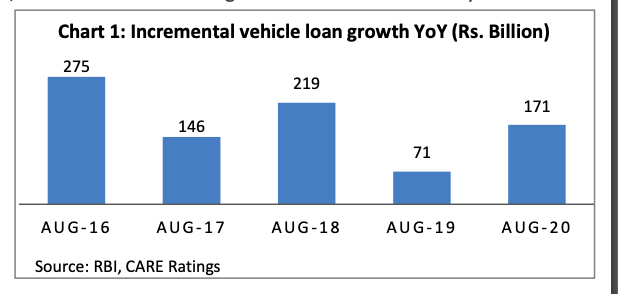

Additionally, vehicle loan interest rates have fallen in recent months, which could help induce vehicle purchases. According to RBI, the outstanding vehicle loans as on 28th August 2020 stood at Rs. 2,197 bn, which is an incremental credit growth of Rs. 171 bn YoY.

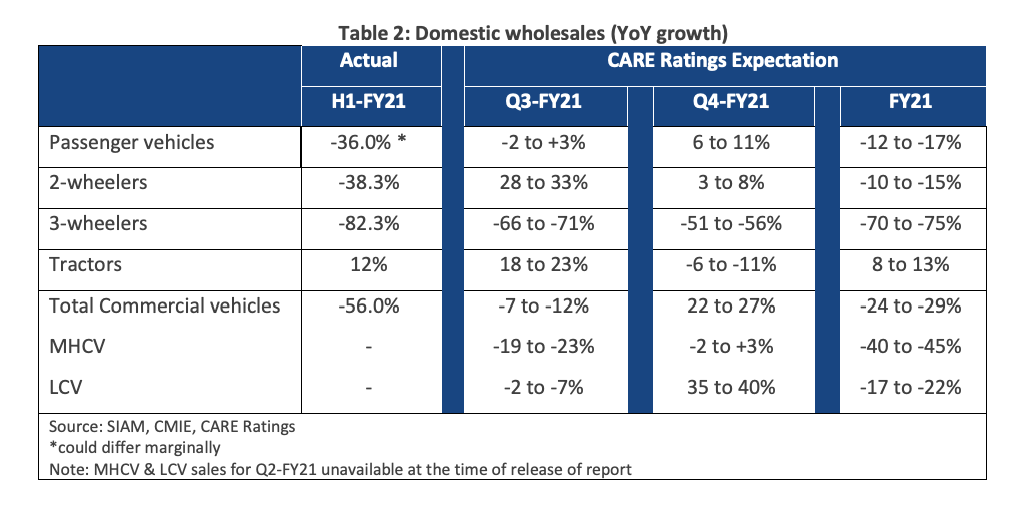

The following table depicts CARE Ratings projections for rest of the year. Domestic sales wholesales shall rise in Q3-FY21, while in Q4-FY21 could be moderated on the assumption that inventory will be high by December 2020 leading to narrowing of wholesales in the last quarter of FY21.

Farm sector

Tractors will be the best performing segment with expected growth in domestic sales of 8 to 13% in FY21, translating to the highest ever sales recorded in history.

The pick-up in CV segment is directly proportional to the economy and the CARE Ratings GDP expectation of -8.1 to -8.2% for FY21 indicates that a complete recovery in CVs, (especially MHCV) domestic sales is unlikely this year. This comes against the backdrop of 28.8% decline in FY20 due to a high base of FY19.