Chennai, NFAPost: India Ratings and Research (Ind-Ra) has estimated banks’ credit costs to range between 2.6%-3.4% in FY21 (2.9%-3.8% for PSBs and 2.0%-2.6% for private banks), depending on the quantum of pool getting restructured or slipping to NPAs.

It has also revised its outlook on the banking sector to Negative for 2HFY21 from Stable. This is in view an expected spike in stressed assets, higher credit costs, weaker earnings on account of interest reversals and lower fee income, and muted growth prospects in the wake of the measures taken to contain the spread of COVID-19.

Additionally, capital buffers for most public sector banks (PSBs) remain modest, As per Ind-Ra’s bear case, the spike in stressed assets due to pandemic is expected to double the credit costs for banking system than estimated pre-COVID-19 levels for FY21.

Negative Outlook on PSBs: The agency has revised the rating outlook on PSBs to Negative for 2HFY21 from Stable. PSBs’ modest capital buffers are expected to deplete further in FY21, due to provisioning requirements. Also, pre-COVID profitability expectations for FY21 would be belied and most banks are likely to report net losses. They may also need to continue to build-up their provision cover in FY22 for restructured assets as some of the restructured assets could turn NPA in FY23. PSBs’ could require Rs 35,000 crore-Rs 55,000 crore in 2HFY21 for Tier 1 ratio of 10%. COVID-19 / contingent provisions are much lower than that for private banks.

Stable Outlook for Private Banks: Ind-Ra has maintained a Stable outlook for private banks, as they are better placed to withstand the challenges presented by the pandemic. Most large banks have strengthened their capital buffers, built contingent provisions and have been proactive in managing the loan portfolio. While the system’s credit growth could remain anaemic, and short-term financial performance could deteriorate modestly, large banks may benefit from credit migration. As opportunities arise, these banks are in a position to gain substantial franchise growth in the medium term, given that they have also added to their capital buffers over the past few months.

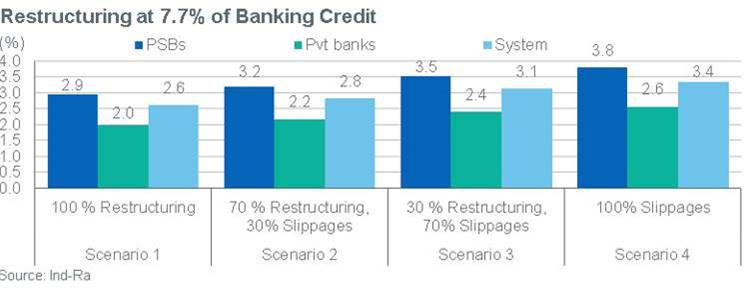

Loan Restructuring Provides Flexibility to Pursue Temporary Relief Measures: Under the new restructuring framework lenders would be able to handhold those borrowers who have been temporarily impacted by COVID-19 but are otherwise viable. Certain stressed assets, though not at the risk of an immediate slippage, could also be restructured. As per Ind-Ra’s estimates, up to 7.7% (Rs 8.4 lakh crore) of the total bank credit at end-March 2020 including corporate and non-corporate segments could get restructured or if they do not qualify for restructuring, they may slip. It could be higher, if the restructuring in non-corporate segments exceeds 1.9% of the total bank credit.

Restructured/Slippages Pool of Rs 3.3 lakh crore – Rs 6.3 lakh crore from Corporates: The restructuring/slippages quantum from the corporate sector in FY21 could range between 3.0%-5.8% of the banking credit amounting to Rs 3.3 lakh crore – Rs 6.3 lakh crore; even stressed assets that may not slip in the near term could be restructured as COVID-19 would have aggravated stress.

Floor for Non-corporate Restructuring at Rs 2.1 lakh crore: With the COVID-19 pandemic impacting all sections of the society, albeit a lower impact on agriculture, the regulator has also extended the restructuring to retail loans as well. The agency now estimates that agri (excluding farm credit) and micro, small and medium enterprises (about 25% of advances in private banks and 32% in PSBs) would contribute about 85% of Rs 2.1 lakh crore (1.9% of banking system credit) non-corporate restructuring, while retail contribute remaining to the restructuring pool.

Restructuring Experience Unpleasant: The experience on restructuring has not been a pleasant one; with peak standard restructured assets at 6% in FY15 – most of it slipped to non-performing categories. However, banks have a guiding framework this time and possibly with better governance framework, and if these guardrails are properly adhered in spirit, Ind-Ra believes the outcome of restructuring process could be far more productive this time around. Nevertheless, even under best circumstances, some restructuring may not achieve success and hence the overhang on asset quality and credit costs would remain elevated in medium to long term, Ind-Ra added.