Chennai, NFAPost: The Reserve Bank of India’s decision allowing lenders to restructure loans would increase their refinancing requirements, especially for non-banking banking companies (NBFCs), says India Ratings and Research (Ind-Ra).

This is in view of their large contractual debt repayments, as scheduled cash inflow gets deferred, though the severity of the same would depend upon the proportion of loan portfolio restructured and terms of restructuring (i.e., complete moratorium vs partial payments).

While restructuring would relieve the repayment pressure on borrowers and can help them to overcome any short-term stress, it would require sound guardrails and critical assessment of viability so that it is not used as an instrument to postpone the problems, as seen previously, Ind-Ra said.

Credit cost pressure gets alleviated since lenders have to provide 10% on the restructured debt. However, this may prove to be inadequate in case the slippages were to be elevated. A higher quantum of restructured assets would clearly reflect higher asset quality challenges for NBFCs and can restrict their ability to mobilise funds from banks ad capital markets.

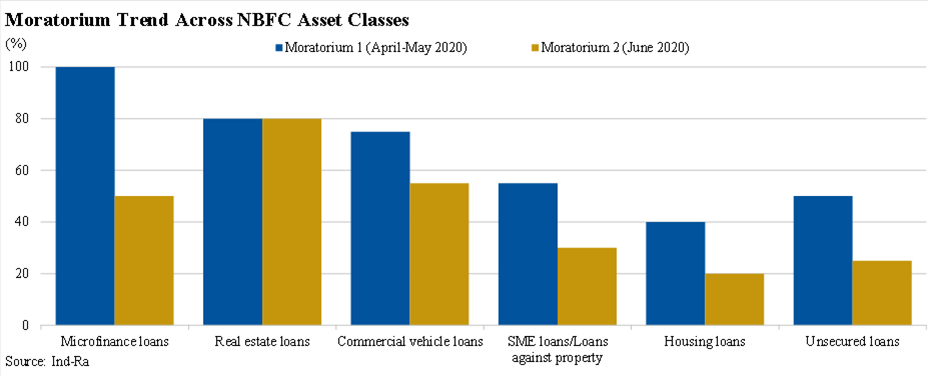

At end June 2020, a substantial portion of the NBFCs loan book was under moratorium. Housing loans had the least portion of the book under moratorium while the wholesale lenders had the maximum portion of their loans under moratorium. The collection efficiency, reflecting the repayment behaviour of customers, has improved since April 2020 with the easing of lockdown restrictions.

However, regional lockdowns did impact collections during July 2020. The collection levels across asset classes / segments were far below pre-COVID levels. Businesses still did not generate cash flows sufficient enough to make their timely debt repayment.

Ind-Ra believes a high proportion of loans to certain segments such as real estate developers, commercial vehicle owners and micro small medium enterprises will be restructured, given the weakness in these sectors.

About 70%-80% of the real estate loans were under moratorium at end-June 2020. Given builders’ cash flows were already weak even prior to the pandemic, due to anemic sales velocity and lack of refinancing opportunities, this book is likely to undergo restructuring first.

Pre-COVID, Ind-Ra had estimated there would be a large portion of real estate-NBFC loans coming out of moratorium in FY21. The restructuring package along with date of commencement of commercial operation extension has brought huge relief for project developers where restructuring with tenor extension up to two years, without classification of account to NPA with board approved policy, would help in providing some breather to the under construction projects which were at deep risk of stalling.

However, there could be asset liability cashflow mismatches for lenders as the asset-side extension would create gaps in their asset liability profile, thereby increasing the importance of carrying a significant proportion of on-balance sheet liquidity and reducing the leverage for a real estate lending business. Also, lenders might have to take material haircuts in some of their exposures to make the restructured proposal commercially viable.

Commercial vehicle players are facing the brunt of reduced freight availability, higher diesel prices and lower freight charges. NBFCs can restructure these loans, given the poor cash flow with these borrowers. However, any extension of the loan tenor could dilute the loan to value (LTV) cover because of the accelerated depreciation of the asset. Lenders may prefer principal moratorium only or rescheduling of cash flows to safeguard LTVs of the exposure. A similar approach may be applied in loan against property/small & medium enterprises’ exposures of NBFCs, the agency said.

Although the restructuring package would help borrowers to manage their debt repayments, it is just a temporary solution to the problem created by the pandemic.

The overall health of NBFCs could improve only with a revival in the underlying economy and the cash flows of borrowers.

The situation as far as the spread of the virus is concerned is extremely dynamic. In case of a second wave of pandemic, the situation may turn grim and borrowers may not be able to meet the restructured debt repayment terms, thereby increasing the credit cost and asset quality pressures, it added.